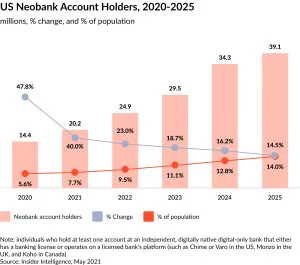

You definitely see that neobanks and mobile banking apps are on meteoric rise today. An urge to start your own fintech business is understandable, and that’s probably why you are here, waiting for the answers on mobile banking app development. Perhaps, you’re expecting “these features and this much money” article, but the JatApp team is going to pour a glass of cold water on you: starting a neobank is a tricky puzzle.

Actually, building your own neobank or mobile banking software solution is a walk through the tightrope over the Grand Canyon. Thinking that you’re the best and you will make it won’t help here, since only few neobanks are expected to become profitable in the near future and even less are profitable today.

Not that many

Sorry for such a harsh introduction which may make you shun away from starting your own neobank. But we have to warn you that this idea is indeed a get rich or die trying situation. But if you’re going to step on that tightrope, don’t you worry, just look into JatApp’s eyes (this article) and keep walking. Our company has been developing fintech products since 2015, so we can take you to the other side of the canyon, where happy customers and investors are waiting for you.

Before you make the first step: neobank definition

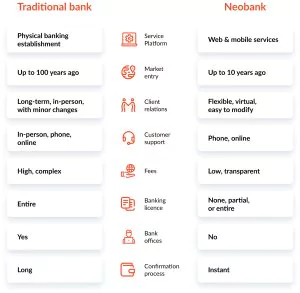

Once starting neobank is a complicated quest, you need to understand clearly what you are going for. Neobanks or challenger banks are digital-only banks that don’t have physical offices and offer core banking services.

There are neobanks that operate as fully registered standalone banks and some that cooperate with incumbent banks that have a banking license. In the latter case, neobanks don’t take care of managing policies that are regulated with the law. Likewise, neobanks partner with conventional banks to use their Automated Teller Machine (ATM) infrastructure to let their customers get cash money without extra fees.

Making first step: technology stack to take a hold of

As soon as you decide to create your own neobank and start mobile banking app development, you have to decide what you will take with you to the other side of the canyon. Of course, we are talking about a technology stack that will actually make your neobank work.

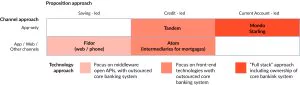

Full-stack neobanks

Don’t get surprised that we started with describing a full-stack approach without saying a word about some “limited” tech stacks. The matter is that there is nothing special to say about opening a full-stack neobank. You just take all responsibilities traditional banks have to carry: security, legal compliance, connection with community banks, expansion of customer base, and so on.

You obviously don’t depend on anyone and that’s why all money is yours, but building a full-fledged infrastructure requires much resources and efforts from the very beginning of your neobank’s life-cycle. Given the circumstances of growing a neobank into a profitable business today, you should be extremely confident that investors will believe in your project and it will pay off.

Neobanks that need third-party infrastructure

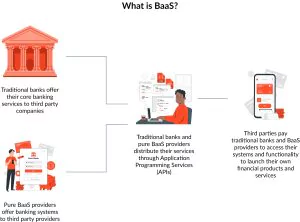

Catering to a third-party infrastructure pushes your neobank towards dependency on so-called Banking-as-a-Service (BaaS) companies, but this approach is much safer. You don’t have to dump money into building the whole infrastructure while your BaaS provider will surely connect you to your customers, community banks, and can even find you other fintech companies to partner with. And you get all this with no hassle related to legal regulations and security management.

You connect your neobank and mobile banking software solution via application programming interface (API) provided by your BaaS company and you’ll have the whole infrastructure in the bag. A typical BaaS provider will charge you a fee for using their platform, or you may share some percentage out of your revenue.

Overall, connecting to BaaS is a risk-free approach that doesn’t let you take the fintech industry by storm, but you have enough time to get your neobank working. On top of that, you can switch to your own banking infrastructure as soon as you see that your neobank is profitable enough.

Balancing in the middle of canyon: problems neobanks face

As we’ve said in the introduction, only several neobanks manage to become profitable today. Once you’re already in the middle of the tightrope, it’s time to think about things that can make your business lose balance and join the majority of failed mobile banking apps on the bottom of fintech Death Valley.

Earnings from low-cost operations

Challenger banks are known for working with underserved populations, which means that high volumes of money are hardly circulating within the neobanks ecosystem. In addition, only a small number of socially secure consumers rely on neobanks as their primary financial service providers.

As a result, neobanks don’t get as much revenue to fuel up their capital for a further growth and adoption of new features and services. Some private investors and venture capitalists keep faithfully believing that investments will deliver returns as soon as a particular neobank presents enough benefits to the consumers.

Unfortunately, this doesn’t happen often because customers don’t see convincing advantages that can entice them to opt for a neobank. Even low usage fees don’t help. Users don’t have any extra reason to make a neobank their primary banking service except for low cost.

As an outcome, neobanks don’t make much revenue, which is why they can’t keep up with incumbent banks that have a lower expenses on customer acquisition but get a way better customer lifetime value. A challenger bank can be proud of a couple of hundred of bucks earned from one customer, while any incumbent gets thousands of dollars from a single account.

Lack of customer engagement

Consumers are reluctant to use mobile banking apps, since low cost is basically the only value proposition neobanks bring to the table. The matter is that neobanks hardly understand what their customers need and aim at only those benefits everyone wants for sure.

To this day, predictability of consumer needs is the main hurdle for making neobanks prosper with a larger number of customers. A mobile banking app may not be enough to churn out thousands of dollars.

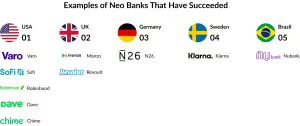

Nevertheless, this rule applies to mobile banking apps that do just mobile banking. If your neobank offers some unique value, getting your profitable customer base is a breeze. We’ll talk about such impressive examples a bit later.

Investor pressure

That could be a good illustration to some anti-capitalist novel depicting evil and greedy capitalists pushing neobanks make money out of nothing. In reality, private investors and venture capital organizations just want to ensure they’ve made the right choice by funding your neobank.

You can find yourself in a situation when everybody expects you to earn a lot of money with just the minimum viable product (MVP) of your neobank, and only your dog understands that running a challenger bank requires patience and determination.

Sadly enough, many entrepreneurs can’t handle this sort of pressure and radicalize their decision making. Remember that building a neobank is a walk on the tightrope over the Grand Canyon? These guys decided to run through it on a monowheel. Just don’t do that.

Incumbent banks rivalry

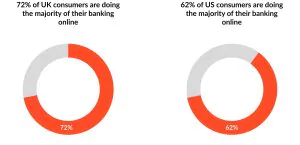

Incumbent banks don’t lag behind and adopt technology to digitalize their services as well, which puts neobanks in a difficult spot. Challenger banks can’t excel in building the same infrastructure and customer acquisition processes as large incumbent banks that just invest enough money in their digital transformation.

Needless to say, the majority of consumers would enjoy the same banking services on their mobile devices, if their regular banks offer such an opportunity.

Incumbent banks going online is a matter of time

Nobody would pick a cat in the sack when they already have something they’ve been trusting for years. Although, the situation isn’t that bad as neobanks have a couple of aces in their sleeves.

What keeps your business alive: neobank business models

Saying that a neobank is just the same as a conventional bank but rolled into a mobile banking app would be a wrong statement, because challenger banks run their own business model. They are similar to traditional banking, but incumbent banks don’t focus solely on one group of services, as they usually bring the whole package.

Neobanks gear towards provision of fewer services, but with better customer centeredness and personalization. That’s your stick for balancing on the tightrope, so read on — we’ll discuss all business models that can be successfully used by challenger banks.

The models are as follows:

- Interchange-led. This business model concentrates on generating revenue made from payment services. When a customer pays for something, a neobank charges them for transferring the payment to a merchant. When a customer uses their credit card, they pay a fee. Chime is the most prominent example of interchange-driven neobank.

- Credit-led. You simply offer your customers a credit card or any similar asset they can use for their own purposes and then return money and interest. In such a way, your neobank generates revenue from interests paid. A common example of that kind of challenger banks is Nubank.

- Asset-led. With this business model, your neobank offers a savings account and deposits that usually have rates much more pleasant than traditional banks’ generocity can allow. Look at Aspiration Bank as an example.

- Ecosystem-led. That’s a business model originally used by challenger banks as they offer bank accounts as a payment hub for other fintech services available. If you have a fintech product of your own, it makes perfect sense to add banking services as the groundwork for your fintech platform. N26 is that type of neobanks that think the same and successfully stake out this business model.

- Product extensions. You may have some non-fintech product that still needs its own banking system to process customer payments. Integrating the whole neobank is a good idea that delivers extra user experience and seamless operations within your application. Amazon does that quite confidently, which means this business model may work for you as well.

What can make you keep moving confidently: improvement tips

The fact that leading a neobank to success isn’t an easy stride through the fintech market doesn’t necessarily mean that there are no ways you can make your challenger bank profitable. We gathered several tips based on the industry insights to give you ideas how you can make your business gain a foothold at the market:

- Powerful standalone unit economics. You should find “your thing” that will be popular with your consumers and sell well as a result. Making banking low-cost is a good strategy, but it has to be some icing on the cake. Remember that you should start making money as early as possible to beat traditional banks in the competition.

- Strong core offering based on digital bank accounts. We’ve mentioned that a low-cost usage fee isn’t always a good strategy to attract new customers, but we can’t say the same about offering other services at a cost lower than average. Again, let’s take the case of Nubank that uses a mobile banking application as the basis, while one of its core services is deposits at a return rate higher than in conventional banks.

- Massive customer acquisition at minimal cost. Even though incumbent banks have an upper hand in the customer acquisition process, you have a lot of ways to attract your own customers. Partnering with other businesses to create a product extension, basic loyalty programs, and prediction of customer financial needs can seriously decrease your customer acquisition costs, thereby unleashing more money for a further scaling and, well, your wallet.

- Focus on a separate customer segment. As soon as you find your target audience, bombard them with offers, because if these people have chosen your neobank, they have a good reason to. They will pay more when you offer them more, just make sure that you’ve detected a genuinely valid group of customers. Think about neobanks that serve freelancers, healthcare providers, small businesses, or any other narrow-specific group of customers.

- Engaging banking propositions. This recommendation overlaps with a tip about maintaining powerful unit economics. You shouldn’t stop at just a mobile banking app. Challenger banks are a much more complicated system that can be armed with a greater range of benefits that are not technology-driven in the first place, but can still be brought to the digital realm. For instance, personal finance management or financial literacy education are the basic examples that can pop up in your mind.

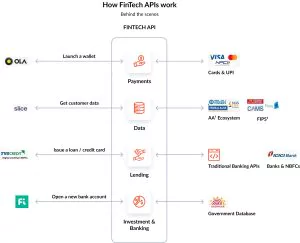

- Reliance on API to access more data and create extra value. Data is a strong enabler of your neobank. You can get tons of data by connecting your neobank to multiple APIs. It’s not just a BaaS-powered scenario, as you can connect your banking app to many businesses, products, services, and organizations beyond the financial sector. Sure, advancing creditworthiness evaluation to provide your customers with a more inclusive loan service will earn you a dozen extra points, but remember that there is much more behind the horizon of the financial sector.

Making the final step: partnering with a vetted technology vendor

Congratulations! You have successfully walked over the canyon, as you’ve learned what business-related and technology issues your neobank will face. However, the last step is to assemble a tech team that will bring your neobank and the mobile banking app to life. JatApp has developed many fintech solutions such as ActivPayroll, bill splitting app, and payment gateway, so our company can build a banking app that will stay ahead of your competitor’s pack.

Start your mobile banking app development by leaving us a note. We will get back to you as soon as possible.